Of course, consternation for the Nashville weather is short-lived when reminded of the destruction of Hurricane Dorian, which made landfall in the Bahamas on September 1st. The category 5 storm left many dead and missing. It will take years to rebuild and the topography has been changed for generations. While of limited solace to Dorian’s victims, the quick and generous response to this tragedy is a reminder that people are charitable, even amidst today’s rapidly changing economic and social landscape.

What season lies ahead for investors is unclear. It should be eventful considering the recognized near-term obstacles, let alone, the long-term. Thus far in 2019 markets have proven resilient. The S&P 500 and MSCI All-World indices are up 20.6% and 16.2%, respectively. As a result, stock investors have recouped the fourth quarter losses of 2018 and then some. Thanks in part to the third quarter rally, bonds are up too with the Barclays Aggregate Bond index gaining 6.4% year-to-date.

That’s right. Bonds and stocks are both posting big gains this year. It’s like a deep snow in Nashville. It can happen, but it’s unusual.

Bulls Versus Bears. The Latest Chapter.

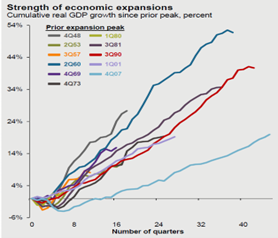

The Bulls remain anchored on stocks’ reasonable price to earnings ratios, especially relative to today’s historically low bond yields. And while long in duration, Bulls foresee an extended recovery noting that the cumulative economic growth for this expansion still lags others by a large magnitude.

Recent wage gains have also helped consumers, particularly lower income households who have heretofore benefited little from the economic recovery. The resulting increased consumer confidence was apparent from the recently reported sales at certain large retailers as well as in the latest housing data. No doubt lower long-term mortgage rates, which fell below 4% for the first time since 2017, contributed to this confidence.

The Bears have their own repository of data and conventional economic wisdom to reference when making their case. They include the trade war’s impact on consumer and business confidence and ultimately economic growth, an inverted yield curve, regulatory and tax policy uncertainty (both at home and abroad), and mounting corporate and government debt balances that only gets worse if interest rates rise. Perhaps not surprising, these macro headwinds have lowered expectations for U.S. public company earnings, which after last year’s 20% growth are now expected to be down year-over-year for the third consecutive quarter.

“Yesterday is gone. Tomorrow has not yet come. We have only today. Let us begin.”

― Mother Theresa

While the Bulls and Bears of Wall Street make their cases for what to expect come tomorrow, the mood among the populace is hardly euphoric. A recent Washington Post poll revealed that 60% of Americans expect a recession in 2020. Economists are a little less gloomy. One-third expect a recession in 2021 according to a National Association for Business Economics survey in August. Consistent with these concerns for the economic cycle, most investors remain overweight defensive and secular growth stories at the expense of more cyclical industrials, financials, and other value stocks. As a result, many companies with attractive and well-covered dividends have been left behind. We’ve been selectively buying some of these stocks, or where appropriate tilting portfolio exposure in that direction via certain exchange traded funds and managers. Put simply, the best opportunities for the future are often those stocks Wall Street has today chosen to ignore.

Seasoned investors understand that economy cycles. The successful ones recognize the limitations of knowing exactly when it cycles. Appreciating these limitations, we have no plans to abandon stocks, including many in the technology and defensive sectors that have outperformed thus far in 2019 and should be part of a diversified portfolio. We will, however, remain sensitive to our clients’ equity exposure relative to their needs and risk tolerances and look to own more or less of stocks depending upon our view of the changing risk versus reward. After all, one thing worse than not being fully invested in a Bull market is being all-in when the Bear arrives.

The Triple-B Market Makes Us a Little Anxious

The Federal Reserve announced another 0.25% rate cut on September 18. The “dot plots,” which are a mechanism the Federal Reserve uses to convey its outlook, are pointing to about a 50/50 chance at one more 0.25% cut before year end. Having started the year yielding 2.7%, the 10-Year Treasury now yields just 1.7%. The yield curve remains flat with a 30-Year yielding just 2.2%. As paltry as these yields are for U.S. government bond buyers, the options remain much worse abroad. In fact, about 30% of global sovereign debt yields a negative rate of interest. That means for $16 trillion of global debt outstanding the lender pays the borrower to use their money!

No one really knows the implications of this historically unprecedented debt picture and how any resulting consequences could unfold. Our fixed-income response to this set of circumstances has been fairly simple. We have stuck with the highest quality credits and sought to limit our risks to higher interest rates by limiting portfolio duration. As the old Wall Street adage goes, we see no reason to “pick up pennies in front of a steam roller.”

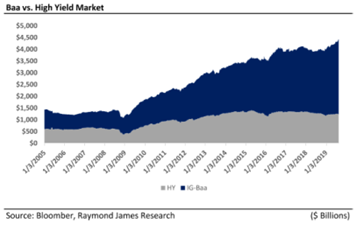

We are particularly sensitive to the risks embedded among lower investment grade credits or Triple-B’s. These issues now represent 63% or $3.2 trillion of all U.S. corporate debt. This growth in Triple-B issues represents a four-fold increase from 2007. Fueling this growth have been investors’ broad-brush treatment of bonds as a safe haven with little regard for quality and price and the flood of money into passive bond funds.

Lower interest rates have helped to reduce the annual interest expense burden for companies carrying loads of debt. Of course, this debt must eventually be repaid or refinanced. If, at that time, issuers find themselves in a season of economic stress or higher interest rates, the pennies the bond investor has been collecting could pale in comparison to the credit losses they might endure.

Repo Rate Spike and Temporary Style Reversal Keep Investors on Their Toes

Most agree that since the Great Recession financial market liquidity has been greatly reduced. New industry regulations and an altered marketplace where passive strategies control considerable pools of assets have contributed to this liquidity reduction. In recent years, this structural change has manifested itself in “flash crashes” in foreign currencies, Treasury bonds, and even large-cap stocks. A few weeks ago the Repo or short-term borrowing market experienced a rate spike to 10% from a typical 2%. This phenomena had many investors on edge for a couple of days. The spike appears to be more a consequence of changing market structures than indicative of wide-spread borrowing fears. Nevertheless, this disruption in overnight borrowing along with some extreme moves within equity style buckets were the latest reminders of how today’s market “pipes” and participants (e.g., more machines and fewer humans) have changed. As for the takeaway, investors better know what they own and why they own it. Otherwise, the next “flash crash” could prove to be an expensive lesson in today’s reduced market liquidity.

WeWork’s IPO Plan Is Not Working. What’s the Implication for the Pipeline?

According to the Wall Street Journal, since 2008 investors have allocated $2 trillion for private investments. We’ve discussed this phenomena and the unappealing implications in previous commentaries.

2019 was going to be the year many of these companies made their public market debut, allowing private growth and buyout equity investors the opportunity to cash out. Most 2019 IPOs have struggled. For instance, with the exception of Beyond Meat (BYND), which is up 500% this year even after losing one-third of its value in recent weeks, Uber (UBER), Lyft (LYFT), and Peloton (PTON) are all trading considerably below their IPO prices. Local sensation, Smile Direct Club (SDC), has seen investors frown on its stock since its IPO priced at $23 on September 11th. It is now trading at $14.

At least these companies managed to complete their IPO’s and in many respects can control their own destiny. WeWork’s parent company We Co., which provides flexible office space among other services, pulled its IPO last week due to a lack of investor demand at a $15 billion valuation. As the largest office tenant in Manhattan, the company raised capital from private investors in January at $47 billion, or more than three times what public investors said was too expensive less than a year later.

“In a bubble, eventually people start saying, 'Wait a minute... these prices are way too high! What is anyone buying anymore? What could they possibly be thinking?' And then there's a correction and a bursting. Robert J. Shiller

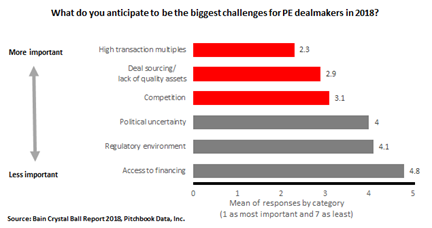

Why weren’t public investors interested in WeWork? To start, last year’s $1.9 billion in losses on $1.8 billion of revenues didn’t help. An eccentric CEO/Chairman, who according to the Atlantic, once claimed the company’s “energy and spirituality” are more important to its success than its revenues and losses, presented another challenge. Investors in other private companies chewing through capital will argue WeWork is not representative. We’d agree WeWork’s prospective IPO was particularly challenged. The evidence, however, increasingly indicates that those allegedly less emotional private equity and debt market investors may be the ones most guilty of losing their valuation discipline in this cycle. Per the Bain survey of private equity participants below, it appears even the industry’s leaders recognize this erosion of valuation discipline.

An Exciting Season at Woodmont

We’re excited to have added three new team members in recent weeks...Grace Bennett, Josh Ireland, and Lindsay Youngbauer. Joining us as Senior Wealth Advisors, Grace and Lindsay are focused on helping Woodmont clients with their investment and wealth planning needs. Josh will oversee operations and identify ways we can capitalize on our firm’s growth and increased scale to continually improve the client experience. You can read more about their impressive credentials and experiences via this link.

Woodmont turns twenty next year. Many clients have worked with us or our predecessor firm for greater than two decades. We are grateful for this longstanding confidence and trust, during both Bull and Bear market seasons. As always, if you have questions or want to sit down for a portfolio review or to construct a financial plan, please let us know.