We approach this topic recognizing how difficult and tenuous evaluating the current situation is. Also, while we were right to recognize this correction felt anything but average, and thus be measured in our desire to increase clients’ equity exposure, that incremental approach and the preservation of cash is of only limited solace given last week’s continued stock declines.

Putting the Price Declines in Historical Context

Following the worst week since 2008, the S&P 500 and All-World Indices are down 28% and 29% year-to-date. The indices have corrected 32% and 30% from the highs just several weeks ago. Value stocks continue to lag the broader indices down 32% year-to-date and 34% from their 2020 peak. Small-cap stocks are now 40% below their peak.

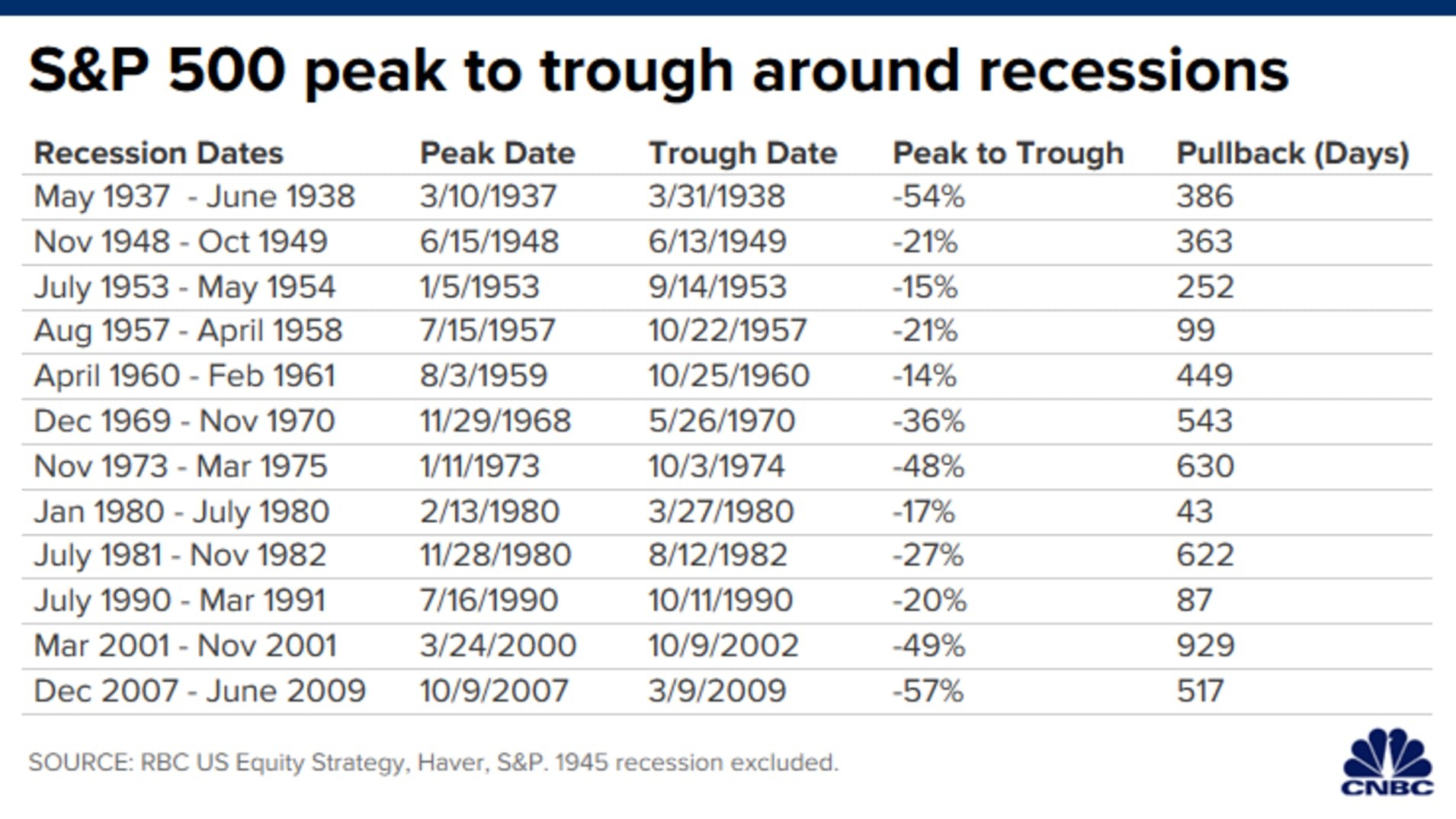

Most economists have concluded COVID-19 will push us into recession (i.e., a period of negative economic growth as measured by our Gross Domestic Product). The table below summarizes historical market pullbacks connected to previous economic recessions. The S&P’s fall since February would mark the fourth worst correction of the last twelve.

Whether the expected recession is short-lived and followed by a steep recovery, or the beginnings of a deeper downturn is the question of the day. Our government’s policy response and, in particular, its ability to help keep capital flowing and cushion the impact on small businesses with limited reserves are crucial variables.

Of course, no one can predict with certainty the length of this likely recession and the associated peak-to-trough market correction. It is interesting to note, however, that in all but one of the recessions since 1937 the market bottomed well before the recession officially ended, reminding us how market recoveries often begin when things still seem dire.

Not Until 2030? That Seems to Us Like An Unlikely Scenario.

The consensus S&P 500 earnings estimate for 2020 has declined 8% in recent weeks to $148. This estimate will continue to come down as companies update their outlooks during the first quarter earnings season beginning in April. The potential 25% hit to second quarter GDP we first referenced a few weeks ago is looking increasingly possible and will weigh on corporate earnings in 2020. In determining whether to own stocks today, however, one must consider what level of earnings beyond 2020 have current stock prices discounted? Put another way, what outcome has the market already priced in and is that forecast reasonable?

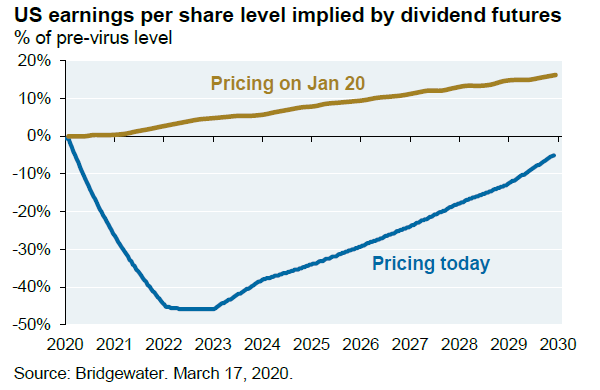

The table below from Bridgewater offers one perspective for how dire a forecast current market prices reflect. Specifically, the chart plots the market price of stocks today compared to January and the implied earnings and dividends trajectory associated with each price. According to Bridgewater, to justify today’s market prices one must assume the S&P earnings and dividends decline nearly 50% over the next two years and won’t recover to the levels we expected as recently as January 2020 until the year 2030. While certainly somber about the unique risks posed by the virus and the measures being taken to fight it, that level of multi-year earnings deterioration and slow-pace of recovery seems like an unlikely scenario.

Another way to think about how much bad news might be already priced in is to consider the most accepted method for valuing companies. That is, the price an investor pays for a stock is the discounted value of that company’s future cash flows. The most immediate four to five years of a company’s future cash flows can represent 30-40% of a stock’s value in this analysis. The earnings in the years beyond can represent the remaining 60% to 70% of its value. Thus, two quarters of no earnings, which is an easy case to envision for many businesses, would be about a 5% impairment to long-term value.

This analysis, of course, assumes companies have the resources to withstand the demand and credit shock that is occurring. Some won’t even with the government’s help considering it will take time for certain consumer and businesses behaviors to return, if at all. We believe, however, the vast majority of large-scale public companies have tremendous staying power. In fact, just as in the 2008/09 Great Recession many of these well-capitalized public companies will come out of the crisis even stronger as they identify new ways to do more with less and some of their weaker competitors don’t make it or are acquired.

The Pennies in Front of the Steam Roller

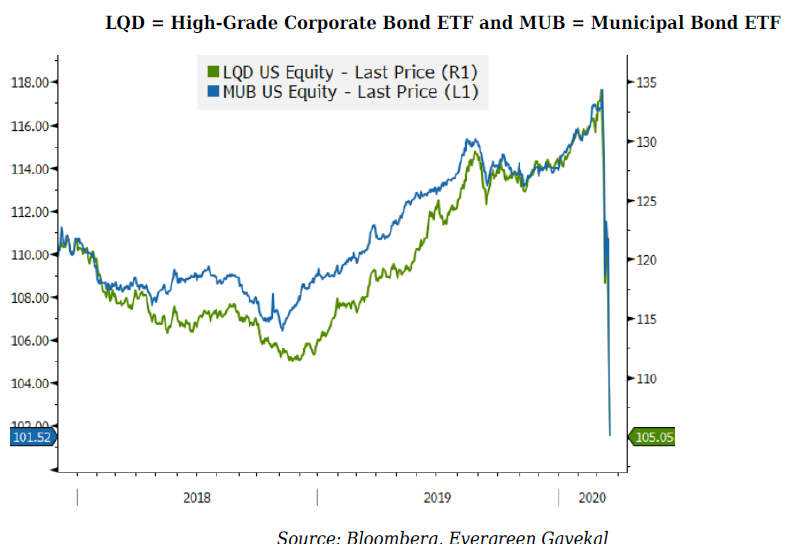

For several years now, we have discussed the risks of reaching for yield by buying certain long-maturity bonds or lower-grade credits. We borrowed the old Wall Street adage “be careful of picking up pennies in front of steam roller” to try to make the point. While holding cash and accepting lower yields in insured bank certificates of deposits or shorter dated maturities limited income in the short run, last week’s bond market action highlighted the risks of that reach for yield. Specifically, as outlined in the chart below, the longer maturity investment grade and municipal bond exchange traded funds fell almost 30% from the highs reached just a few weeks ago.

We are now looking intently for those opportunities where the yield and more specifically the spreads between the risk-free rate of return and the return offered by these corporate and municipal securities is compelling. Regardless, we remain sensitive to credit quality given the difficultly of quantifying today’s economic risks, and our bias to limit our risk taking to equities. After all, the upside for a stock can be multiples over long periods of time. Whereas, for a bond the best you can do is earn some interest and get your money back when the bond matures.

Short-Lived or A Long-Term Downturn?

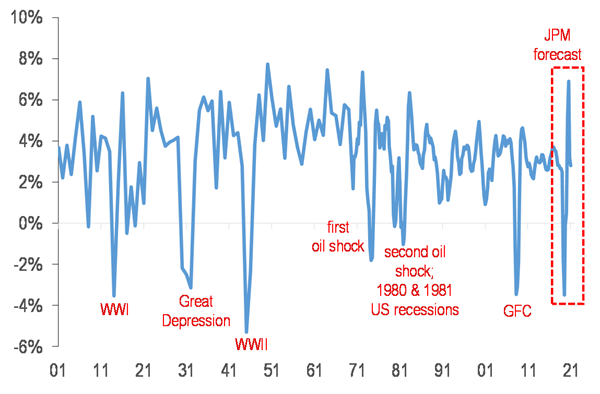

Economists and market strategists are offering a wide range of forecasts regarding the implications for the current economic shutdown and potential stimulus package, the likes of which we have never seen. Some maintain we could see a quick and deep contraction only to be followed by an unusually strong recovery in the second half of 2020 and in 2021. The chart below from JP Morgan depicts one such view. Others fear a recession so deep with job losses and credit carnage that it will take our economy years to recover.

Source: JP Morgan

As for stocks, we may not know for many more weeks whether the market declines in recent weeks were efficiently discounting a long-term economic decline in which corporate earnings do not recover for many years. Or, as Warren Buffett explained in his 2016 annual letter, this is one of those every decade or so opportunities when “dark clouds will fill the economic skies, and they will briefly rain gold. When downpours of that sort occur, it is imperative that we rush outdoors carrying washtubs, not teaspoons.” While the “washtubs” approach is only appropriate for our most risk tolerant and equity-centric clients, we continue to appreciate Buffett’s perspective for how buying stocks at lower prices to hold for the long-term reduces not increases the risks associated with owning them.

Thank you for your continued trust and confidence during what has proven an unnerving and difficult time at home and around the globe. We remain hopeful for our ability to slow the spread of this virus and are particularly grateful for the thousands of care givers and first responders making sacrifices to serve so many so well.

As always, if you have questions or we can be of assistance, please do not hesitate to contact us via email or phone. In the meantime, be safe and try to enjoy some of the spring season, which the weekend’s warmer weather reminded us is just around the corner. Warmer weather? Considering it might help fight the virus, it cannot get here soon enough.