Happy Birthday, America!

Americans love an underdog. This summer, we’re cheering for Cape Verde (pop. 0.5 million) in the World Cup in addition to the U.S. team. We’re rooting for those first-generation college engineering graduates and support staff, who took a risk and traded salary for equity in their recently or soon-to-be “IPO’d” start-ups. And, finally, the ultimate underdog movie, “Rocky,” is again in the news thanks to some notoriety around the timing of the original’s release. Arriving in theatres in late 1976, it coincided with our nation’s bicentennial. This was also a time when America needed a theatrical, not to mention economic, pick-me-up.

"Every champion was once a contender that refused to give up."

Rocky Balboa

Perhaps this love affair is a product of our founding. Thirteen small and hardly cohesive colonies declared independence from the mighty British Empire. The founders put forth a compelling vision and listed plenty of grievances in the Declaration of Independence. Yet, few could have predicted that a disparate Continental Army (and eventually some key allies) would defeat the British Army. The fact that this experiment in Democracy turns 250 on Saturday only adds to America’s Cinderella story.“I have found–as I am sure you have, in your travels–that people everywhere, in spite of occasional disappointments, look to us–not to our wealth or power, but to the splendor of our ideals.”

President John F. Kennedy

The United States is no longer an underdog. Far from perfect, we have plenty going for us. We have tremendous natural and intellectual resources, and our capitalistic system rewards ingenuity, hard work, and risk-taking. Elected officials either adapt to the people’s will or are relatively quickly ousted. A poorly swinging pendulum (and there have been plenty in U.S. history) can only swing for so long. (source: WSJ, Harvey Mansfield: America is 250 Years Young) Moreover, as our World Cup visitors have reminded us, America is not what you see on cable news and in the depths of the internet. Americans are generally gracious, industrious, and naturally curious. “I am a firm believer in the people. If given the truth, they can be depended upon to meet any national crisis.”

President Abraham Lincoln

We will need all of these traits to navigate the long list of domestic and geopolitical tests ahead. Given the fiscal challenge highlighted by the U.S. Debt to GDP ratio, which recently eclipsed World War II levels, we must also learn not to “judge policies and programs by their intentions rather than their results.” (Milton Friedman, 1912-2006). Regardless, when we get down on ourselves, as recent survey data suggest, it is good that our friends from abroad have reminded us how fortunate we are. Earnings Growth Has Proven a Powerful Tailwind for the S&P 500

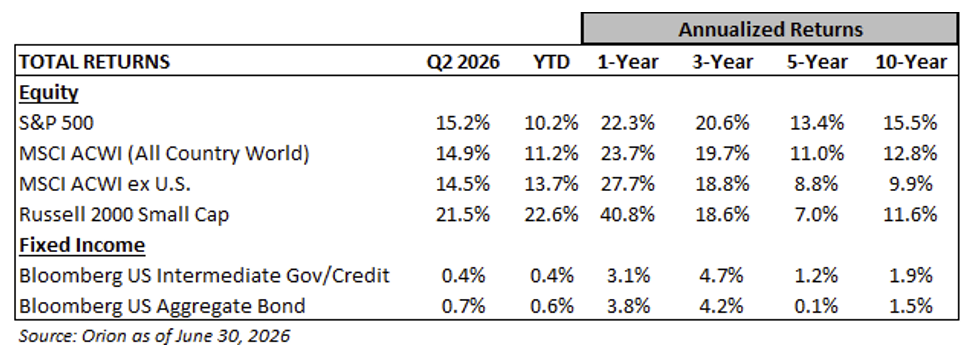

As of early March, the consensus 2026 earnings growth forecast for the S&P 500 was 15%. Today, expectations are for 25%, thanks in large part to the index’s record-setting profit margins and strong trends for Communication Services, Consumer Discretionary, Technology, and Materials, all of which reported over 40% growth to start the year. (Source: FactSet) The anticipated strength for 2026 follows an already heady period with S&P 500 annualized earnings growth of 15% from 2020 to 2025. Put another way, if companies achieve this year’s current earnings target, S&P 500 earnings will have increased two-fold in just the past five years. This doubling of earnings provided a lot of fuel for the stock gains of recent years.

Entering the second half of 2026, equity investors’ focus on the 2027 earnings outlook will increase. While much can change given today’s dynamic landscape, current expectations are for another 17% increase. The trend of strong earnings is why the S&P 500 is up 10% for the first half of 2026. Yet, at 21.7X and 18.6X, the price-to-earnings ratios for 2026 and 2027 are below where we started the year.

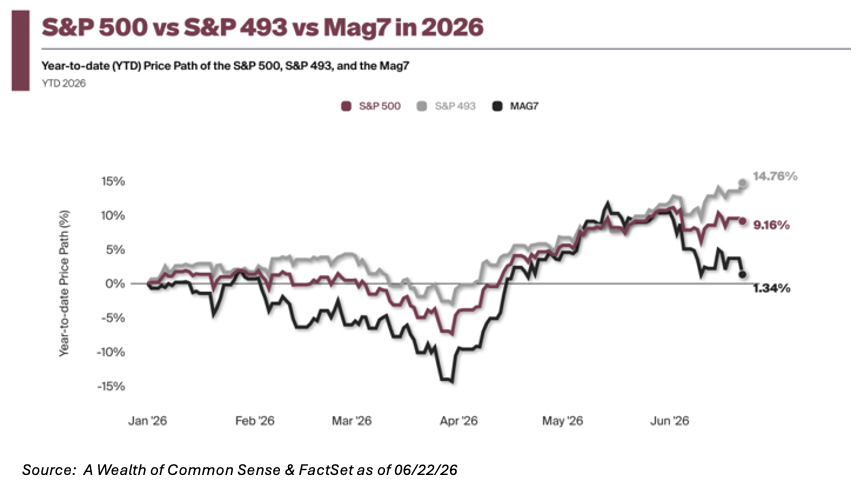

We have discussed the economic tailwinds of the historic AI expansion and capital investment in recent commentaries. The expansion investment thesis remains mostly intact, despite growing angst as current spending levels require increasing amounts of capital (debt and equity). Fortunately, for diversified investors, the market gains have broadened beyond the Magnificent 7 and a handful of other AI winners. Industrials, energy, materials, consumer staples, and real estate were all up 10% or more in the first half of the year. Whereas the Magnificent 7, representing 33% of the S&P 500 capitalization after years of strong gains, gained less than 1%.

Strength Beyond U.S. Large Caps and the Mag 7

Despite traditionally struggling in a rising interest rate environment, small and mid-capitalization stocks posted significant gains in the first half of 2026, up 22% and 16%, respectively. Some worry speculative excess, including significant investor fund flows into newly formed double and triple-leveraged ETFs, has pushed short-term investors down the capitalization spectrum. Others see outsized efficiency benefits as smaller enterprises integrate exciting AI innovations. While a case can be made for both, small and mid-capitalization stock allocations remain an important part of a diversified portfolio, albeit a natural underweight for income-centric or risk-averse investors.After lagging for nine years, non-U.S. stocks had another strong period, up 14% year-to-date. Non-U.S. stocks have now outperformed the S&P 500 by 7% since the fall of 2024. The U.S. Dollar’s relative decline since early 2025 and the closing of the P/E gap between U.S. and non-U.S. equities have contributed to this turnaround. It also helped that the South Korean stock market (now 7.9% of the ex-U.S. index) has doubled year-to-date on the strength of a handful of semiconductor and memory chip suppliers.

The relative valuation discount for non-U.S. stocks compared to U.S. stocks has narrowed to 33% from a peak of 47% in 2024. The average discount is around 20%. This existing gap is worth noting. Our interest in maintaining non-U.S. equity exposure, however, is less about the discount and more a recognition of the value of diversification amidst shifting global trade patterns and heightened geopolitical tensions.

New Federal Reserve Chair Warsh’s First Test

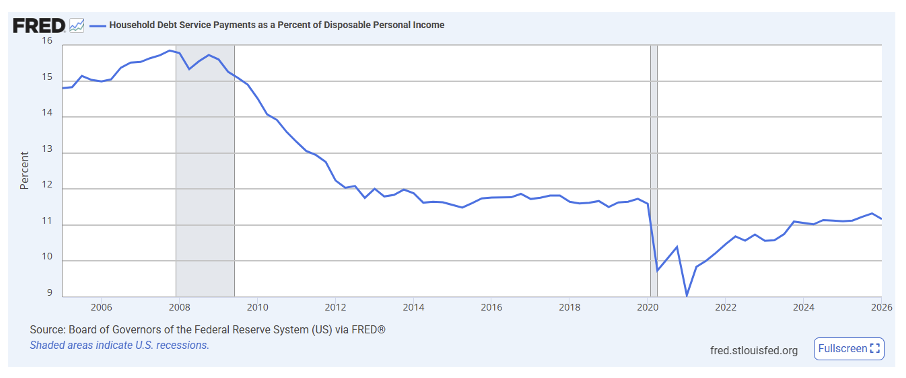

Bond and equity investors have been debating for months the implications of Chair Warsh taking the helm at the Federal Reserve. Following the June 16-17th Federal Reserve meeting and press conference, the topics worth debating had narrowed. Importantly, Chair Warsh has no plans to ignore inflation in favor of politically expedient rate cuts, a move that displayed an important level of independence at the start of his tenure. Moreover, investors should expect Warsh and colleagues to heed Aaron Burr’s advice to Alexander Hamilton to “talk less and smile more.” In other words, the Federal Reserve wants to avoid diluting its messaging power by overcommunicating.Interest rates moved higher on the heels of the June meeting. Warsh’s pledge to “deliver price stability” was viewed as hawkish. Also, the economic data, including employment, capital spending, and manufacturing, have proven resilient, especially amidst uncertainty surrounding the war in Iran. The consumer, who has endured a gas price spike, vacation travel inflation, and the threat of AI job losses, has yet to experience a dramatic deterioration in economic circumstances. In fact, household debt service remains below 2019 levels and, according to JPMorgan, the consumer cash pile is at a record $22.9 trillion compared to $14.8 trillion pre-COVID.

Heading into the second half of the year, bond markets anticipate a Federal Funds rate increase of 0.3% versus expectations for a December rate cut as recently as April. While today’s higher rates won’t help the housing market (the U.S. Ten-Year Treasury at 4.4% is up from 4.2% at the start of the year and 3.6% two years ago this fall), consumers continue to forge ahead, defying many economic oddsmakers and the recent consumer sentiment data.

Given the potential volatility of the economic landscape, including the risks that inflationary pressures persist, we have not materially altered our conservative approach to managing fixed-income portfolios. While the recent increase in interest rates and wider spreads afforded us a window to modestly increase portfolio duration and broaden our credit exposure, the focus remains on owning investment-grade government and corporate bonds with a typical portfolio duration of 3 to 3.5 years, which remains well below the intermediate U.S. government/credit benchmark’s 5.7 years.

AI Is Not Free! Are the Costs Worth It?

Three years ago, our July Market Commentary was titled “Hot Dogs, Apple Pie, and AI.” As much as AI had emerged as an exciting investment theme midway through 2023, it is startling to compare this year’s estimated $800 billion of “build-out” investments with the $70 billion of three years ago. (source: Goldman Sachs and Stanford University) Never mind how rudimentary the early ChatGPT offering was versus Anthropic’s latest Claude model and other emerging inference solutions.

Despite the AI investments and innovations of the past three years, some significant challenges remain. First, we still do not have a long-term plan to power these solutions. While more energy-efficient models should emerge, access to power (and the associated expense) remains a limiting factor to adoption. The growing “not in my backyard” data center phenomenon is certainly connected to this energy obstacle.

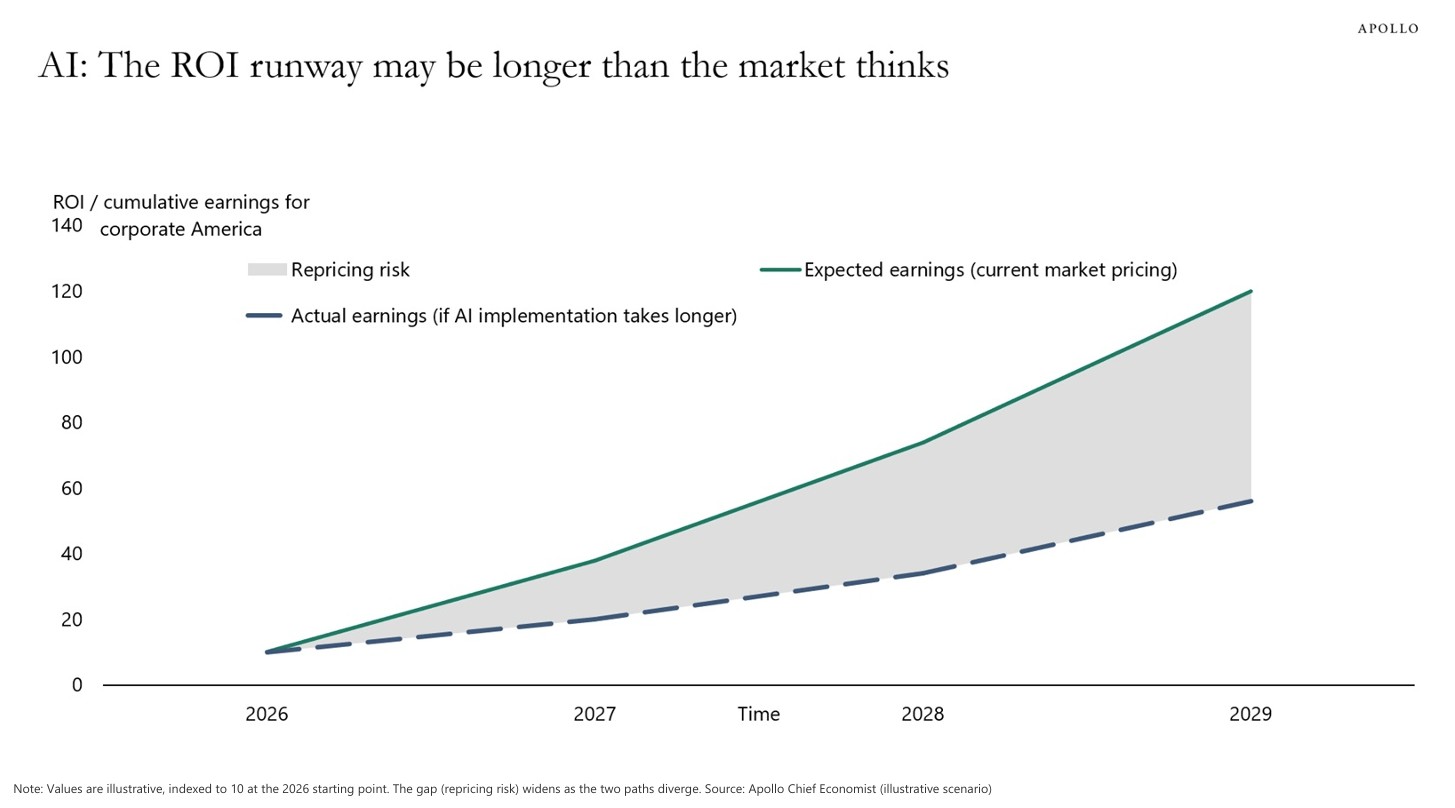

Second, the AI customer value proposition is unclear. In a recent report, Apollo Global Management noted that the benefits of AI integration for many tech and software companies are reasonably apparent. Yet, for almost every other sector, the current costs are far too high for the expected enterprise savings or performance benefits. As companies renegotiate AI vendor contracts this summer, the challenge of this expense line item is increasingly apparent.

Third, we must balance the excitement for AI access and proficiency with the cognitive and developmental downsides. We all recall the long-term benefits (educational and emotional) from “grinding it out” over a demanding analysis or good old-fashioned trial-and-error creativity. AI shifted the landscape so quickly, including at our colleges and universities, that we are behind in discerning when it is actually helpful.

Few dispute that the long-term market for AI solutions is massive. Yet the costs, compared to the benefits, have emerged as an obstacle to adoption. And, much like the eventual parental and institutional revelations about mobile device use, the odds are increasing that AI access for our youth will not go unfettered. These new near-term adoption headwinds could, in turn, negatively impact AI-company valuations and their access to capital, both of which have experienced few restraints since our “Hot Dogs, Apple Pie, and AI” in July of 2023.

Year 251 Angst? A Comprehensive Financial Plan Can Help.

An easy news query reveals plenty of data pointing to Americans’ deteriorating trust in government, concerns for the economic outlook, and declines in “personal happiness.” Rural or Urban, Democrat or Republican, High or Low Income, Americans are worried about the future. As we have discussed before, part of this heightened anxiety stems from the media’s efforts to engage us. Bad news elicits more clicks than good. Another part of this dissatisfaction is life’s fast pace, which can too often disconnect us from friends, neighbors, and institutions that ground us.

There is no easy cure for these challenges. However, in our experience, a comprehensive financial plan and tax and estate strategies can narrow the variables and provide a clearer financial picture, possibly reducing some degree of angst. If you have not taken advantage of these services, year 251 is a great time to start.

“If I can change, you can change, everybody can change!” – Rocky Balboa

As always, thank you for your continued confidence and trust. We look forward to answering your questions and wish you a wonderful 4th of July holiday.

The Woodmont Team

July 2, 2026

This document contains general information only and is not intended to be relied upon as a forecast, research, investment advice, or a recommendation, offer, or solicitation to buy or sell any securities or to adopt any investment strategy. The information does not take into account any reader’s financial circumstances or risk tolerance. An assessment should be made as to whether the information is appropriate for you with regard to your objectives, financial situation, present and future needs.

The opinions expressed are of the date of publication and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and non-proprietary sources deemed by Woodmont to be reliable, are not necessarily all inclusive and are not guaranteed as to accuracy. There is no guarantee that any forecasts made will come to fruition. Any investments named within this material may not necessarily be held in any accounts managed by Woodmont. Reliance upon information in this material is at the sole discretion of the reader. Past performance is no guarantee of future results.