Topics:

- Do I need to enroll in Medicare when I turn age 65?

- When is Open Enrollment for Medicare?

- What happens when I retire from my employer after age 65?

- What is the difference between Traditional Medicare and Medicare Advantage?

- What does Medicare Part A cover, and how much does it cost?

- What does Medicare Part B cover, and how much does it cost?

- What does Medicare Part D cover, and how much does it cost?

- What does Medicare not cover?

- What is Medigap Insurance, and when should you buy it?

- Considerations When Comparing Traditional Medicare vs Medicare Advantage?

- What are health insurance options for Retirees under Age 65?

- What should I consider when changing plans?

- Available Resources

Do I need to enroll in Medicare when I turn age 65?

When you turn 65, Medicare will become the primary payer unless you are continuing to work and your employer has 20 or more employees. In this case, you may not need to enroll in Medicare, and your employer health coverage generally remains the primary payer. On January 1, 2025, new rules took effect requiring insurance carriers to perform a review and calculations to determine if their health insurance plans PASS or FAIL as “creditable.” It is always recommended to check with your HR department or benefits broker to ensure your employer's plan is a "Pass." If not, you will want to enroll in Medicare to avoid late enrollment penalties.

When is Open Enrollment for Medicare?

Medicare open enrollment occurs annually, October 15th through December 7th. This is when Medicare users can choose to re-evaluate part of their Medicare Coverage (Medicare Advantage/Part C and/or Part D Plan) and compare to other plans on the market. After re-evaluating, if there is a plan that better fits one’s circumstances, there is an option to switch, drop, or add a Medicare Advantage and/or Part D plan.

Important Considerations: When switching from Medicare Advantage to Traditional Medicare, your access to Medigap coverage depends on whether you have guaranteed issue rights.

If You HAVE Guaranteed Issue Rights:

- You can buy certain Medigap policies without medical underwriting

- Insurers cannot deny you, charge more, or impose waiting periods for pre-existing conditions

- You qualify if you’re within 12 months of joining Medicare Advantage and had a Medigap policy before

- You also qualify in specific situations, like: your plan is ending, you moved out of the service area, or the company misled you

If You DON’T HAVE Guaranteed Issue Rights:

- Insurers can use medical underwriting and may deny you coverage based on your health

- You may face higher premiums or be rejected entirely

- If you are rejected, you’ll be responsible for Traditional Medicare’s 20% coinsurance with no annual out-of-pocket limit

- You’ll need to purchase a separate Part D prescription drug plan

Bottom line: If you don’t have guaranteed issue rights, switching could leave you without supplemental coverage and facing unlimited out-of-pocket costs. It’s essential to consult with a licensed insurance agent before making this decision.

For those interested in Medicare Advantage Plans, open enrollment is January 1st through March 31st.

The initial enrollment period for an individual approaching age 65 is seven months long. This includes the three months prior to your 65th birthday, the month of your birthday, and the three months following your 65th birthday.

What happens when I retire from my employer after age 65?

If you did not enroll in Medicare because you continued working for an employer that had 20 or more employees but are now retiring, you will have a special enrollment period. The special enrollment period is an eight-month period that begins after the employment ends or your employer's health insurance coverage ends (whichever occurs first).

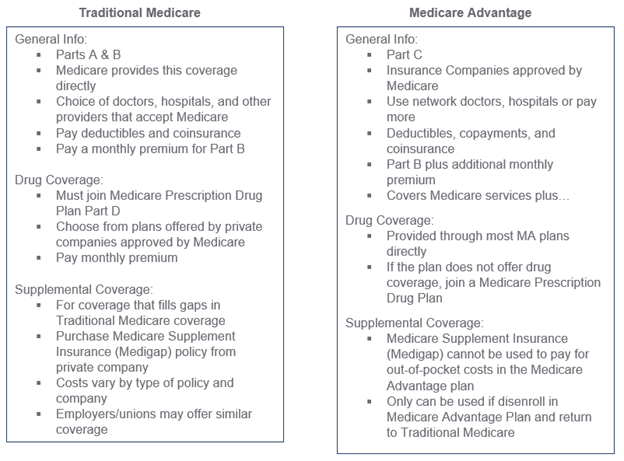

What is the difference between Traditional Medicare and Medicare Advantage?

Source: Medicare.gov

What does Medicare Part A cover, and how much does it cost?

Medicare Part A, known as Hospital Insurance, covers the following:

- Inpatient hospital care

- Skilled nursing facility care (if certain conditions are met and coverage is for a limited time)

- Some home healthcare

- Hospice care

- Inpatient psychiatric care

Medicare Part A is considered “premium free” if you or your spouse paid Medicare taxes for a certain amount of time while working.

What does Medicare Part B cover, and how much does it cost?

Medicare Part B, known as Medical Insurance, covers the following:

- Doctor’s services

- Outpatient services

- Some home healthcare

- Durable medical equipment and supplies

- Certain preventive care

- Ambulance services

- Outpatient medical and surgical procedures

Medicare Part B premiums are automatically deducted from your benefits plan including:

- Social Security

- Railroad Retirement Board

- Office Personnel Management

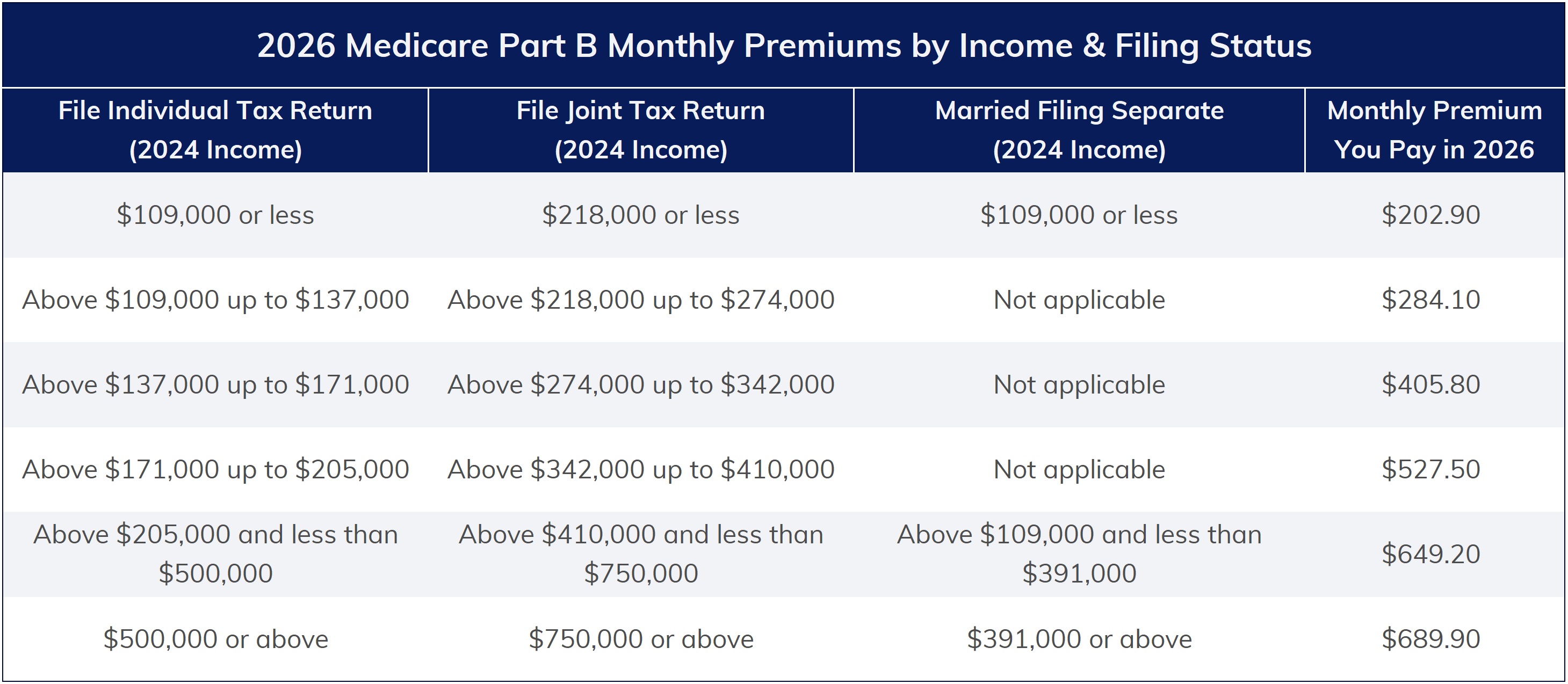

Medicare uses the Modified Adjusted Gross Income (MAGI) reported on your IRS tax return from two years ago. If your MAGI from two years ago was above a certain amount, you will also pay an Income Related Monthly Adjustment Amount (IRMAA), which is an extra charge to your added premium.

Source: Medicare.gov

Source: Medicare.govMedicare Part B also has a deductible of $283 in 2026 that must be met. After you meet the deductible for the year, you typically pay 20% of the Medicare-approved amount for these:

- Most doctor services (including while you are in the hospital as an inpatient)

- Outpatient therapy

- Durable medical equipment

What does Medicare Part D cover, and how much does it cost?

Medicare Part D, known as Prescription Drug Coverage, varies by plan. Each plan must give at least a standard level of coverage set by Medicare. Plans can vary the list of prescription drugs they cover (called a formulary) and how they place the drugs into different “tiers” on their formularies.

Medicare Part D premiums are automatically deducted from your benefits plan including:

- Social Security

- Railroad Retirement Board

- Office Personnel Management

Medicare uses the Modified Adjusted Gross Income (MAGI) reported on your IRS tax return from two years ago. If your MAGI from two years ago was above a certain amount, you will also pay an Income Related Monthly Adjustment Amount (IRMAA), which is an extra charge to your added premium.

Source: Medicare.gov

Source: Medicare.govBeginning in 2025 and continuing in 2026, Medicare Part D includes an annual out-of-pocket spending cap. For 2026, once you spend $2,100 on covered prescription drugs, you will pay nothing for additional covered drugs for the remainder of the year. This cap provides significant protection against catastrophic drug costs. The $2,100 cap does NOT include your monthly Part D premiums or IRMAA surcharges, which you continue to pay throughout the year regardless of your prescription drug spending.

Starting January 1, 2026, Medicare's new drug price negotiation authority takes effect for the first time. Ten commonly used high-cost medications will be available at significantly lower negotiated prices. If you take any of these medications, you may see substantial cost savings in 2026. Contact your Medicare plan for specific pricing information.

You can review the latest information about this new negotiated pricing and the 10 drugs included in the first round of negotiations by visiting: CMS.gov

What does Medicare not cover?

Medicare does not cover:

- Most dental care

- Eye examinations related to glasses

- Dentures

- Cosmetic surgery

- Acupuncture

- Hearing aids and exams for fitting them

- Long-term care

What is Medigap Insurance, and when should you buy it?

Medigap insurance is a Medicare Supplement that covers gaps in Traditional Medicare coverage. Medigap does not cover services not covered by Medicare. You must be enrolled in Traditional Medicare to get Medigap Insurance.

Medigap enrollment is 6 months from the first day of the month of turning 65, assuming one plans to enroll in Medicare. No medical underwriting is required with this initial enrollment period. Exception: for other periods that allow for “guaranteed issue rights” medical underwriting may be required. After age 66, individuals wanting to switch from a Medicare Advantage plan will need to undergo medical underwriting.

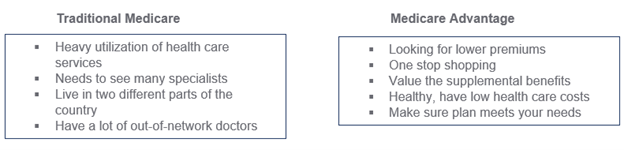

Considerations When Comparing Traditional Medicare vs Medicare Advantage?

Source: Medicare.gov

What are health insurance options for Retirees under Age 65?

- Spousal Coverage

- Employer-provided retiree coverage

- COBRA

- Affordable Care Act Marketplace

What should I consider when changing plans?

When you are thinking of changing your plan, consider the following:

- Review suitability of Medicare Part D plans each year

- Review suitability of Medicare Advantage plans each year

- Challenges in buying a Medigap policy outside of open enrollment period

- Before disenrolling from a Medicare Advantage plan, find and enroll in a Part D plan and a Medicare Supplement (Medigap)

When comparing available options, consider the following:

- What are the premiums?

- What are the deductibles and coinsurance payments?

- Is there a maximum limit on out-of-pocket costs?

- Are current doctors and hospitals used covered under this plan?

- How often do premiums change?

- Are prescription drugs covered?

- Does the plan offer dental, vision, and/or hearing coverage?

Available Resources

You can find more information on Medicare.Gov. Medicare provides online tools for choosing plans and provides a phone line for support. In addition, please feel free to call us with any questions. If we cannot answer your questions, we can identify a Medicare expert to help navigate this complex landscape. Woodmont Investment Counsel is a fee-only advisor. We do not sell insurance or receive compensation for referrals to insurance agents.

This document contains general information only and is not intended to be relied upon as a forecast, research, investment advice, or a recommendation, offer, or solicitation to buy or sell any securities or to adopt any investment strategy. The information does not take into account any reader’s financial circumstances or risk tolerance. An assessment should be made as to whether the information is appropriate for you with regard to your objectives, financial situation, present and future needs.

The opinions expressed are of the date of publication and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and non-proprietary sources deemed by Woodmont to be reliable, are not necessarily all inclusive and are not guaranteed as to accuracy. There is no guarantee that any forecasts made will come to fruition. Any investments named within this material may not necessarily be held in any accounts managed by Woodmont. Reliance upon information in this material is at the sole discretion of the reader. Past performance is no guarantee of future results.