There is no shortage of challenges for investors to digest as of late. The war in Ukraine, U.S. debt downgrade, political dysfunction by most anyone’s measure, and 7.8% mortgage rates have all contributed to the tenuous environment. Mix in heightened labor tensions, government shutdown prospects, and $100 oil forecasts, and it is easy to understand JP Morgan CEO Jamie Dimon’s pronouncement last month that “the uncertainties out there ahead of us are still very large, and very dangerous.”

Fortunately, it is not all bad news. Nor is it the first time the well-respected CEO has warned of an economic “hurricane.” As for the positive, enthusiasm for AI’s potential to improve lives and not destroy them continues to mount, GLP-1 diabetes and weight-loss medications are currently making life better for millions, and the investment pipeline for onshoring manufacturing and infrastructure is large.

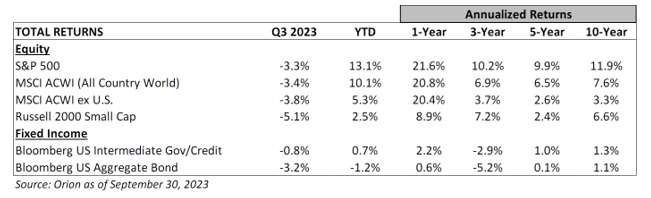

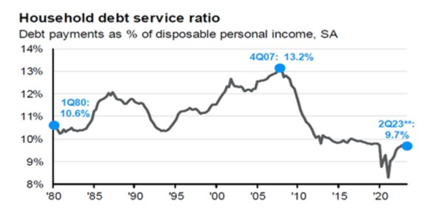

These positive developments are long-arc opportunities that could drive considerable economic activity and improve our quality of life for years to come. And while more recently household excess savings have dwindled, consumer debt service is below historic levels and savers who are paying attention now earn 4% to 5% on their FDIC-insured deposits.

Source: JP Morgan, September 2023

As for the news headlines, we will cover a few of the high-profile topics of the day in this commentary, including the recent government shutdown drama and record Federal deficits and debt. We will also discuss some of our nation’s historic challenges leaning on the insights of an August Wall Street Journal opinion piece, which makes the case that as bad as the political polarization is today, things have been far worse before.

Unfortunately, we cannot assure you the news flow improves anytime soon, or that the issues won’t grow worse before getting better. We are hopeful, however, that a review of current market conditions and some of the challenges from previous eras provide a contextual respite for the understandably weary investors among us.

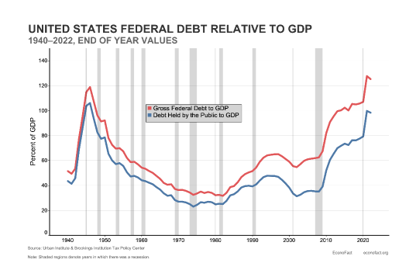

Federal Debt Ratios Return to Historical Peaks

A government shutdown was narrowly averted late Saturday evening. The deal pushed out the next likely funding tussle all the way to mid-November.

There have been 10 government shutdowns since 1980, the most recent of which was in late 2018 and lasted for 34 days. Part of the issue is a once laborious and detailed budget process that involved Congressional committee “work,” or at least some oversight, has given way to passing Continuing Resolutions. These Continuing Resolutions combine every expenditure into one up or down vote. Highlighting the unfortunate nature of this trend, former Speaker Pelosi openly confessed “you have to pass the bill so that you can find out what is in it.” While Speaker Pelosi’s quote best captures the Congressional dysfunction, both parties are guilty of failing to run a budget process.

Thanks in part to the Continuing Resolution scapegoat, and the sacred nature of entitlement programs, government deficits have become the norm, adding to our nation’s now $33 trillion in debt. We’ve previously discussed the challenge of this mounting debt, which to make matters worse doesn’t account for unfunded Medicare and Social Security entitlement obligations.

The ratio of a nation’s debt to Gross Domestic Product (GDP) is one metric investors following government debt monitor closely. For years, even though we were running deficits and piling on debt, many economists considered these levels manageable given a debt to GDP ratio below 100%. While the metric ignores the impact higher borrowing costs have on fiscal deficits (e.g., a two-year Treasury pays 5.1% today versus a 3.1% long-term average), the fact the ratio was still below peak levels offered some degree of comfort.

Around 2012, our debt to GDP ratio moved back above 100%. Earlier this decade, it eclipsed post World War II levels of 120%. This development has caused many to consider what happened post World War II that enabled a return to ratios under 40% by the 1960s. The answer is primarily two things – GDP growth and above trend inflation.

With inflation persistently trending above the Federal Reserve’s 2% target and significant stimulus related to COVID-19 initiatives and the Inflation Reduction Act clean energy bill in the system, one can’t help but wonder if inflation is the playbook for our current debt to GDP dilemma. If so, investors can expect continued pressure on fixed-income prices and lost purchasing power for savers.

"Inflation is the one form of taxation that can be imposed without legislation." Milton Friedman

While we won’t know about the playbook until after the fact, the threat adds yet another reason why we have refrained from extending fixed-income duration beyond five years and remain content to invest in short and intermediate-term bonds. The threat that this latest bout of inflation could be more structural and thus last for years is also why we believe equity and other capital appreciation strategies should continue to be an important part of most clients’ diversified portfolios.

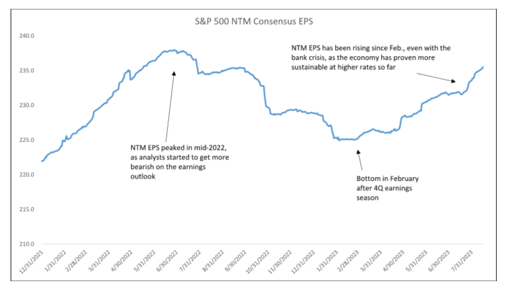

A Stealth Recovery in the Outlook for Corporate Earnings

The chart below highlights how the next twelve-month earnings expectations declined 5% from mid-2022 to February 2023 and then have recovered steadily since. There are plenty of obstacles to sustaining this earnings recovery, not the least of which are much higher borrowing costs for consumers and companies alike. We will know more in the coming weeks as companies report third quarter earnings and update their forecasts.

Nevertheless, the recovery in the earnings outlook points to a surprisingly resilient economy in the face of higher interest rates. It also highlights the nimbleness of many major corporations to preserve margins and earnings. This nimbleness is consistent with the idea that quality companies tend to get stronger in periods of economic challenge and disruption. And despite seemingly more frequent C-Suite and Board-room shenanigans, we are encouraged that U.S. corporations continue to lead the world in innovation and capital stewardship.

Source: Raymond James & Associates

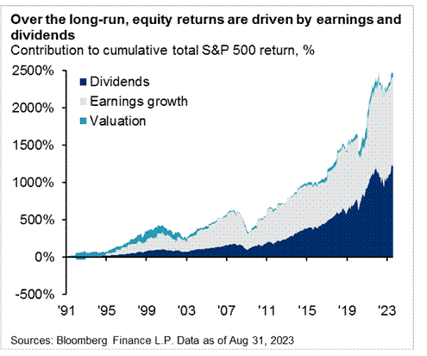

Earnings Growth + Dividends = A Compelling Long-Term Investor Combination

It is important that most investors, and certainly those with a long-term investment horizon, have exposure to both growth-focused and value or dividend-focused equities. Going all-in on one or the other could work wonderfully in a given year. Yet as the wide dispersions of performance in 2022 when value outperformed growth and vice versa thus far in 2023 demonstrate, investors run the risks of missing periods of significant gains if they concentrate on one and neglect the other.

Regardless of a company’s growth or value style, two factors will drive long-term returns: earnings and dividends. While there are periods such as the late 1990s and 2000 when investor euphoria boosts stock prices, ultimately stock gains are tethered to these fundamental factors.

The S&P 500 trades at 19X and 17X 2023 and 2024 estimated earnings compared to a twenty-five-year average of 17X. Some argue the current premium and today’s higher rates mean that in the years ahead earnings and dividends must carry more weight to offset a potential contraction in equity valuations. Fortunately, for investors, most stocks are trading at price to earnings ratios at or below historical averages. For example, the P/E ratio for the S&P 500 excluding its ten largest stocks is just 14X. Similarly, mid-cap, small-cap, and non-U.S. stocks are far from expensive. And while small-cap earnings tend to suffer greater than large-caps in periods of recession and rising rates, the average small-cap stocks 40% decline from its peak points to considerable bad news already reflected in current prices.

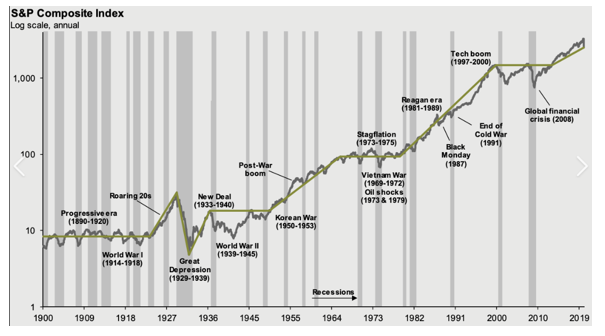

Not Our First Rodeo

Most are familiar with the old Wall Street adage that “markets climb a wall of worry.” The current news flow and regular client inquiries about the extent of today’s challenges caused us to dig it up for this commentary.

Source: Standard & Poors

As you know, today’s wall of worry is full of the bricks of political polarization and excess government debt. And while we believe the Internet and social media exaggerate our current divisions, an emerging distrust of the capitalist system that has enabled successive generations to live better than the one before is certainly concerning. These challenges beg the question whether this wall proves too steep. It is a legitimate question and one we do not easily dismiss.

A review of some of our nation’s more tumultuous times is a helpful reminder for investors that this is “not our first rodeo.” The August Wall Street Journal piece, “America Is Often a Divided Nation,” by Karl Rowe was most insightful in this regard. Specifically, Mr. Rowe listed decades of examples to support his thesis that as bad as the divisions are today, we’ve been through much worse. For instance, the 1960s and 1970s saw a nation bitterly divided over civil rights and the Vietnam War. These divisions contributed to hundreds of destructive riots in our major cities, the assassination of leaders, two Presidents effectively driven from office, protests on college campuses, an assault on the Pentagon, and in 1972, as many as 2,500 domestic bombings. Source: Wall Street Journal, Rowe, 8/25/23

“U.S. politics today is ugly and broken, true enough. But the good news is that it was worse in the past, and it will get better again.” Karl Rowe, Wall Street Journal, August 25, 2023

We know many of you lived through the long list of 1960s and 1970s turmoil and tragedy Mr. Rowe cited. And some of you have experience with the challenges of the 1930s, a decade where at one point one in four Americans was out of work. According to historian Wendy Wall, who was cited in Rowe’s piece, the 1930s was “marked by sit-down strikes, violent repression of workers, and attacks by vigilante groups on Jews, Catholics, racial minorities, and leftists.” Moreover, populism was the political tool of the day and the communist party gained momentum, albeit short lived. Suffice it to say, this was not a nostalgic, let alone, promising period.

As for some context for today’s political blood sport, between 1874 to 1904, Rowe explained how the controlling party of the House, which regularly flip flopped during this period, expelled 62 members of the opposition party on often suspect charges. This record doesn’t excuse many of today’s tactics, but the deep distrust of the opposition certainly seems to have that historical “rhyme” scholars regularly reference.

"Forgive your enemies, but never forget their names." President John F. Kennedy

We recognize history offers limited solace for anyone suffering from today’s trials and tribulations. Yet in the light of the broader strokes of the historical brush, it is comforting to know the weary have found periods of rest. And while we may have to wait for this next period, remember that investors who look beyond the day’s headlines and hold on during the volatile times, will be rewarded.

A Larger Office in a New Location

In the spring of 2011, we moved Woodmont’s offices downtown. We signed an attractive lease, secured enough space for growth, and hoped the downtown location sent a message that we were ready to serve clients throughout the Middle Tennessee region.

Fast forward twelve years later and we need more space having grown from six to sixteen. As a result, at the end of October we are eager to move to our new office location on Bedford Avenue near the Green Hills Mall. While we will miss the excitement of the downtown corridor, none of us will miss the current ingress and egress challenges.

We will soon contact you with more details related to the office move and other administrative initiatives we believe will help us better serve you. In the meantime, please do not hesitate to contact us with questions about your portfolio or financial plan. Thank you for your continued trust and confidence and best wishes for a wonderful fall season.

The Woodmont Team

October 2, 2023