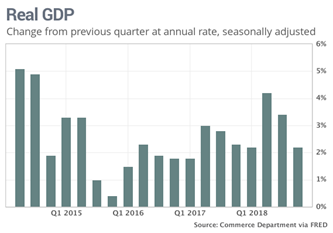

This weather maelstrom, a government shutdown, ongoing trade tensions, and a Brexit mess, have likely depressed first quarter U.S. and global economic activity. We’ll soon know more as companies begin reporting first quarter earnings and the government’s economic data estimates are released. In March, we learned the U.S. economy grew just 2.2% in the fourth quarter versus an initial 2.6% estimate. The trillion dollar question is whether this growth slowdown is temporal or if it portends a coming end to the second largest economic expansion on record.

Despite the nasty weather and a long list of worries, the S&P 500 notched its best first quarter since 1998 gaining 13.6%, and now up an impressive 21% from its low on December 24th. U.S. stocks remain remarkably resilient, reminding investors of the difficulty of betting against “The American Tailwind” Warren Buffett referenced in his recent Berkshire Hathaway annual letter, not to mention a very accommodative Federal Reserve. The first quarter’s big gains also speak to how poorly the market performed late last year. In fact, even after the strong start to 2019, the S&P 500 is still 3.5% below its all-time high set in October. Small-cap stocks are 11.5% from their highs. International stocks, which outperformed during the fourth quarter market sell-off, lagged the S&P 500 in the first quarter with the Ex-U.S. All-World Index up 9.4%. Thanks in large part to that accommodative Federal Reserve, bonds rallied resulting in a 2.3% gain for the Barclays Aggregate Bond Index.

The wild ride of the past six months brings to mind two important investment maxims, both of which we have no doubt referenced before. First, the “stock market is like a roller coaster, you get hurt if you jump off.” Second, to offset any percentage market decline, it takes a larger percentage gain. To crystalize this fact, start with 100, take away 20%, add back 20%, and note it leaves you with 96.

We recognize the tension between these two investment truisms, especially for clients with shorter investment horizons or a desire to limit volatility. Put another way, some investors are more willing or capable of riding the roller coaster (i.e., taking more risk) for the potential of bigger gains. To help clients gauge their stomach for the ride, in this commentary we discuss current stock and bond valuations and some of the factors we believe could meaningfully push prices up or down. Considering the significant personal data that floats around during tax season, we also share some important reminders regarding good cyber security practices, which can never be too top of mind in the cloud-based world in which we operate.

Multiple Expansion “Lyfts” Stocks in the First Quarter

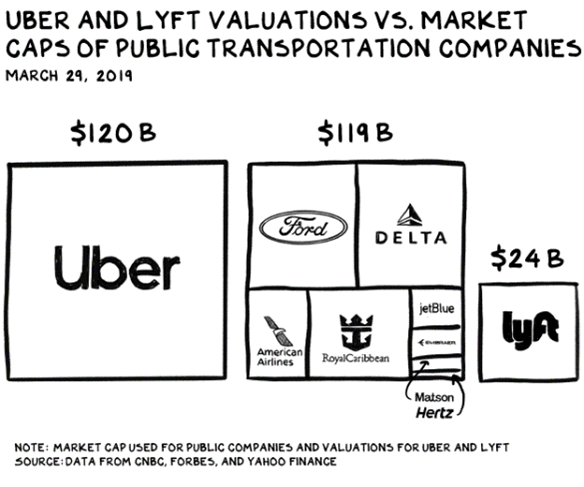

On Friday, ride-sharing company Lyft went public ending the day with a $26.5 billion valuation. The company lost $900 million in 2018 and is expected to lose money for years to come. Yet a “$1.2 trillion total addressable market (TAM)” is an enticing story for aggressive growth investors. Management and the IPO bankers believe this TAM will be divided up between Uber and Lyft much like Verizon and AT&T share the nationwide cellular market.

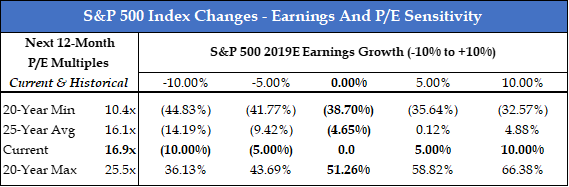

The stock market is a compilation of emerging businesses like Lyft with a huge TAM and massive losses, or Verizon and AT&T, both mature companies with modest growth prospects but well covered dividends yielding 4.1% and 6.4%, respectively. While we always welcome a discussion regarding why we own or do not own certain companies, for purposes of this commentary, however, we’re going to discuss the market tide that often lifts or sinks investor boats. Consider, for instance, at the beginning of the year market strategists were forecasting $173 in 2019 S&P 500 earnings. Today, the consensus estimate is $167. Stocks enjoyed strong gains in the quarter despite these earnings revisions because the price investors decided to pay for that expected stream of S&P 500 company earnings (i.e., the P/E) increased from just shy of 14X at year end to 16.9X today. While earnings must grow to drive value over time, the P/E that investors are willing to pay typically represents a more significant variable for stock prices.

Currently, the S&P 500 is trading just above the 25-year average P/E, but the historical range for twenty year averages is rather extreme at 10.4X to 25.5X. When investors fear earnings peaks or can find less risky income sources elsewhere, the P/E comes down. On the flip side, investors may pay a higher price if they believe current estimates are too low, or there are few alternatives in the bond market or elsewhere. For instance, advocates for the stock/bond relative valuation methodology argue our current low-interest rate environment supports a P/E multiple in the high 30s. Using this framework, international stocks would be even cheaper on a relative basis at 13.7X earnings.

Source: WIC & FactSet

Depending upon the multiple that investors will pay for earnings, the market outlook can vary greatly up or down. To understand this take a minute to study the large percentage changes in the table above. Unfortunately, there is no specific data set to help us pinpoint the appropriate P/E for a period in time, which is why stock investors must be prepared for the inevitable ups and downs that come with owning stocks.

An Inverted Yield Curve: Something Simply to Note or to Fear?

Investors generally insist on more return on their investment the longer the investment commitment period. In U.S. government credit markets, this relationship is illustrated by what is historically a steepening yield curve (i.e., yields go up as maturity dates increase). As a result of the Federal Reserve and other global central bankers’ efforts to try to stimulate economic activity by keeping long-term interest rates historically low, the curve has been unusually flat for years. During the first quarter, however, the yield curve inverted in places. Specifically, earlier in March the Ten-Year U.S. Treasury Bond yield fell below the 3-month T-Bill. This followed inversion of the 3-month T-Bill and 2-Year Treasury Bond in January.

The yield curve remains steep compared to past inversions (e.g., the all-important 10-Year to 2-Year Treasury spread is still positive). Yet, the recent development has investors on edge considering since the 1960s a U.S. recession has followed seven of the last eight yield curve inversions.

Not surprisingly, inversion extrapolations for moves in the stock market are difficult. First, a near-term recession is not inevitable. Second, the average time lapse between inversion and when a recession did develop is 17 months with stocks often enjoying significant gains post curve inversion. Third, there could be unusual factors contributing to this recent inversion. For instance, J.P. Morgan highlights renewed deflationary pressures and the re-pricing of global quantitative easing (i.e., how much more U.S. government bonds yield relative to the practically 0% investors can earn in Europe). And this is theoretically positive for equities as the P/E multiple may expand to account for less attractive fixed-income investment options. After all, it was just a few months ago markets were worried about a 3% Ten-Year siphoning funds from stocks and into cash and fixed-income.

Suffice it to say, economists’ and market strategists’ predictions for this latest inversion are wide-ranging. While always leery of the “this time is different” explanation, we can appreciate today’s unusual circumstances and how it could affect the predictive power of this inversion. Nevertheless, we’ll stop well shy of concluding economies no longer cycle and thus continue to hold some cash or cash equivalents for that rainy day when the economy stalls and markets get sloppy.

Some Investor Fear (Or At Least a Healthy Dose of Re-Positioning) Is Already Here

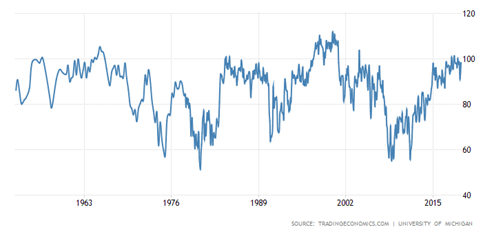

We’ve always been interested in survey data that provides insight into the sentiment of consumers, business owners, and investors. Generally speaking, poor sentiment correlates to cheaper asset prices (or at least less competition for those assets) and thus more long-term upside for investors willing to look beyond the day’s gloom. Upon reviewing the recent data, there is nothing that points to sentiment depression. We’re also far from any enthusiasm peaks. The long-term chart below of the University of Michigan’s sentiment survey is indicative of where consumers currently sit on the historical spectrum. Business and investor survey data reveal similar emotions – not too hot and not too cold. Of course, anecdotally, we would be hard pressed to conclude trade tensions, heated political rhetoric, mounting government debt, and fear for how technology is quickly changing the jobs and opportunity landscape have not taken a meaningful toll on the sentiment of anyone reading the papers, let alone, those active on social media.

Consumer Sentiment Survey through March 2019

Considering the fair to middling signals of the sentiment data, stock market performance data and investor positioning are particularly noteworthy. Specifically, defensive stocks have outperformed cyclical stocks (e.g., Utility stocks are up 9% and the Dow Transports down 13% this past year), equity fund flows are negative, the dollar is strong, and long/short hedge funds haven’t been this hedged since 2016. Combining the sentiment and market data, it appears the recession that an inverted yield curve may signal has been anticipated to some extent.

“Passwords are like underwear: make them personal, make them exotic, and change them on a regular basis.” — overheard at SecureWorld Atlanta

Unfortunately, cyber breaches and identity theft are far too common for large and small companies and individuals alike. Cyber thieves continue to get better at disguising their favorite schemes such as email phishing, formjacking, and malware. They also continue to find new avenues to steal our identity, including secretly watching your every move on your personal computer.

As a reminder, you should not send us personal information via an unsecured email or a login we have not discussed. If you ever receive an unsolicited email from your custodian or a Woodmont team member asking to confirm or send personal information, please call us. You are likely under attack. For other important tips, see this link. In the meantime, change your passwords often and be creative, if not exotic.

A First Quarter to Remember

Astonishing stories from the recent college admissions scandal, tragic developments associated with Boeing’s 737 Max design, and our firm’s support for an event to raise awareness of Colon Cancer have reminded us of life’s unpredictability and been cause for a more contemplative first quarter than we admittedly expected. As you ponder and address life’s triumphs, tragedies, and the daily curve balls, please know we are here to serve as a resource and your financial partner so that you can focus on other important life pursuits. Thank you for your continued confidence and trust. We look forward to answering your investment and wealth management questions and wish you a wonderful spring season.